Introduction

Real estate referrals can be powerful when it comes to growing your business. They help you expand your network and serve clients more effectively. In one survey, 87% of agents said they earned referral income in the previous year.

However, while referral fees are common in the industry, they can also create challenges when it comes to tracking payments, staying compliant, and keeping everyone on the same page.

To put the numbers into perspective, the current average home sale price in the U.S. is about $368,581. If the commission on one side of the transaction is 5%, that equals 18,429.05. With a 25% referral fee, the referral agent or broker would earn $4,607.26 just for making the connection.

That's a significant amount of money to manage, especially when multiple referrals are happening across different deals.

The problem is that referral fees can easily slip through the cracks without a clear process in place. Mismanaged agreements, missed payments, or compliance oversights don't just strain professional relationships; they can impact your bottom line.

In this article, we'll unpack what real estate referral fees are, how they work, and some best practices for agreements. We'll also discuss the best solution for managing and tracking referral fees to simplify your operations.

What Are Real Estate Referral Fees?

A real estate referral fee is a commission paid to a licensed real estate agent or broker who refers a client to another agent or broker.

When agents refer clients, the fee compensates them or the broker for connecting a buyer or seller with a real estate professional who ultimately handles the transaction.

Typically, the real estate agent or broker who receives the referred client pays the referral fee from their commission after closing the transaction.

The typical Realtor receives approximately one-quarter of their income from real estate referral fees, highlighting their importance.

An example of referral fees

Let's unpack an example of how a referral fee would work:

- A receiving agent closes a $500,000 home sale with a 3% commission, which works out to $15,000.

- The referral fee is 25%, so $3,750 goes to the referring real estate agent.

- The referring agent's brokerage may take a portion of the fee, depending on their split agreement.

How Do Real Estate Referral Fees Work?

Referral fees typically follow a structured system to ensure proper compensation, transparency, and legal compliance. Below is a breakdown of how real estate referral fees work:

1. Identifying a referral opportunity

A real estate agent or broker, known as the referring agent, may come across a client who needs services they can't provide.

This could be a buyer or seller moving to a different city or state, or a client seeking a specialized real estate service, such as luxury or commercial properties.

Instead of turning the client away, the referring agent connects them with another real estate agent or broker, known as the receiving agent, who can help.

2. Finding the right real estate agent to refer

The referring agent looks for a trusted real estate professional in the target market or niche. This can be done through:

- Personal or professional networks.

- Brokerage affiliations.

- Online agent directories or recommendations from colleagues.

- Real estate conferences and networking events.

One real estate agent or broker typically conducts due diligence to ensure the receiving agent is competent and reliable since their reputation is on the line.

3. Negotiating and signing the referral agreement

Before passing the client along, the agents or brokers draft a referral fee arrangement, which typically includes:

- Referral fee percentage: A typical referral fee is 20% to 30% of the receiving agent's commission. However, there is no standard referral fee rate for brokerages.

- Payment terms: When and how the fee will be paid, such as after closing the deal.

- Client ownership: Ensuring the referring agent or broker doesn't interfere once the referral is made.

- Expiration date: The time frame in which the referral must convert into a deal.

4. Connecting the client with the receiving agent or broker

Once the agreement is in place, the referring agent or broker introduces the client to the receiving agent.

There is typically a client handover with relevant details about their needs and preferences, which is when the referring agent's involvement ends unless agreed otherwise.

5. The receiving agent or broker closes the transaction

The receiving agent or broker takes over, working with the referred client to buy or sell a property. Their goal is to complete the transaction successfully so they can earn a commission and fulfill the referral agreement.

6. Paying the referral fee after closing

Once the transaction is finalized, the receiving agent gets their commission from their broker.

At this point, the receiving agent's broker deducts the referral fee from their commission. The fee is then sent to the referring agent's brokerage, and the agent gets paid after the brokerage processes the payment.

Best Practices for Structuring Real Estate Referral Agreements

Structuring a real estate referral agreement correctly ensures that everyone understands their obligations, prevents disputes, and ensures compliance with legal and ethical standards.

Let's unpack some best practices for structuring a solid referral agreement:

Use a written agreement

A written referral agreement is essential to avoid misunderstandings and legal issues. Verbal agreements are risky and may not be enforceable in court. Always draft a formal agreement, even for referrals within the same real estate business.

Your written contract should outline who is involved, what the obligations are, and how payment will be handled.

It's a good idea to use industry-standard referral agreement templates from your local real estate board or legal counsel.

Include key contract terms

A comprehensive referral agreement should include:

- Parties involved: The full legal names and license numbers, contact details, and signatures of both brokers.

- Client details: The name of the referred client and the type of transaction, such as buyer, seller, or landlord.

- Referral fee amount and structure: Clearly state the referral fee structure and how it'll be calculated, such as a flat fee or percentage.

- Payment terms: Outline when the fee is due, if the receiving agent pays it, what happens if the deal falls through, and how payment will be made.

- An expiration clause: This defines the duration of the agreement.

- Exclusivity clause: Some referral agreements specify whether the referred client is exclusive to the receiving agent.

Ensure compliance

You should ensure that you check state-specific laws when drafting your referral agreement.

For example, Iowa doesn't allow out-of-state agents to collect referral fees unless they're licensed in the state.

Clearly define the scope of work

The referral agreement should define the responsibilities of both agents or brokers. These responsibilities could include:

- The referring agent shouldn't interfere once the client is handed off.

- The receiving agent should update the referring agent on the transaction status.

Verify and track referral payments

You should document the referral process by keeping records of signed agreements, emails, and payment confirmations. One way to do this is by using Paperless Pipeline's Commission Module (more on this shortly).

Can Transaction Coordinators (TCs) Earn Referral Fees?

While transaction coordinators (TCs) play a very important role in real estate transactions by managing paperwork and deadlines, there are strict legal and ethical limitations when it comes to them earning referral fees.

Whether a TC can receive a referral fee depends on state licensing laws, brokerage policies, and federal regulations like RESPA.

In most cases, TCs can't earn referral fees unless they hold an active real estate license. The key reason for this restriction is that referring a client in exchange for a fee is considered a real estate activity, which typically requires licensing.

If a TC has an active real estate license and works under a broker, they can legally receive a referral fee, provided it's paid through their brokerage.

Key Legal and Compliance Considerations for Real Estate Brokers

Real estate brokers must navigate a complex legal landscape when dealing with referral fees to ensure compliance with state laws, federal regulations, and industry ethics.

Failure to follow these rules can result in fines, a suspended license, or legal action.

Here are some key legal and compliance considerations for brokers when it comes to real estate referral fees:

State laws and licensing requirements

When it comes to referral fees, the rules aren't the same everywhere. In most U.S. states, you can also receive referral fees if you're a licensed real estate broker or agent. It's generally illegal to pay an unlicensed real estate professional for sending business your way.

Typically, these fees move from broker to broker, not directly between agents. Even if an agent sets up the referral, it's the broker of record who has to handle the paperwork and make sure everything is above board.

Some states go even further by putting limits on referral fees, requiring extra disclosures, or banning them in certain cases, like in some rental transactions.

In many places, agents also need to be upfront with clients about referral arrangements. For example, in Florida, brokers must tell clients about referral fees if the client asks.

Federal laws

The Real Estate Settlement Procedures Act (RESPA) is a critical federal law regulating referral fees.

RESPA Section 8 states that referral fees between brokers are legal, but payments between agents and third parties, such as lenders or title companies, are often illegal kickbacks.

An example would be that a mortgage lender can't pay a real estate agent a referral fee for sending them a client.

Penalties for violating RESPA can result in fines of up to $10,00 per violation, civil lawsuits, and loss of license.

Cross-border and international referral fees

Some states require both the referring and receiving agents to be licensed in that state to collect a fee legally. An out-of-state agent may collect a referral fee without a local license in other states.

For example, in California, an out-of-state agent can earn a referral fee provided they're licensed in their home state.

International referrals involve additional tax implications and foreign real estate laws, so the referring broker must ensure that the receiving broker follows local licensing laws in their country.

Currency exchange rates and tax reporting may also impact cross-border payments.

Ethical considerations

The National Association of REALTORS® (NAR) Code of Ethics sets ethical standards for referral fees.

The NAR requires Realtors to fully disclose referral fees to clients if they receive compensation from another party. The client should also understand that the referral is not purely based on service quality but involves a financial incentive.

It could be considered unethical if a referral is made solely for financial gain rather than for the client's needs.

According to the Code, the best practice is to clearly explain to the client why the referred agent was chosen, whether it's their market expertise or specialization.

Tax considerations

Referral fees must be reported as taxable income by both brokers. In the U.S., referral fees are usually reported as 1099 income (if independent contractors) or W-2 income (if salaried).

Tax withholding rules may apply if you're referring an agent outside the U.S., and some international transactions require Form W-8BEN (for foreign individuals receiving U.S. income).

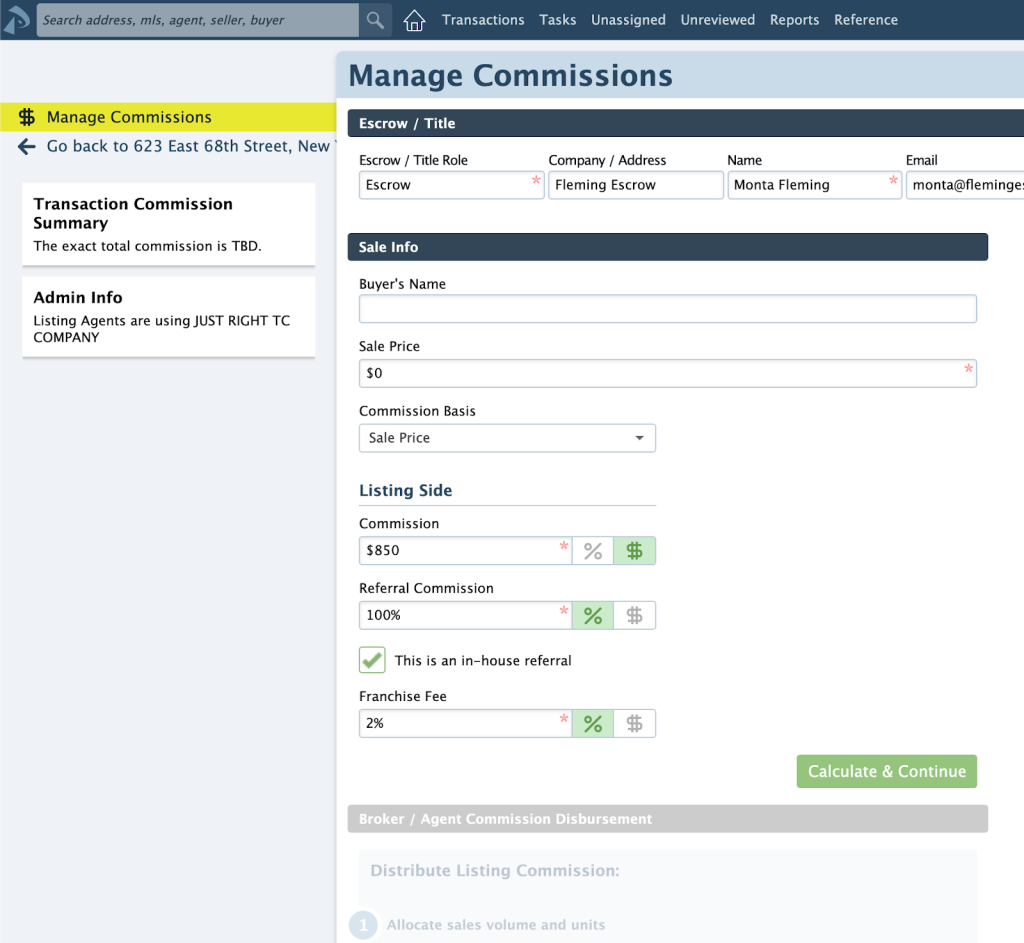

How to Track and Manage Referral Fees Efficiently with Our Commission Module

Our Commission Module is a powerful tool for tracking and managing real estate referral fees. Here's how the platform can be used to handle referral fees effectively:

Automating referral fee calculations

When entering a transaction in Paperless Pipeline, you can add a referral fee as a deduction from the total commission. The system allows you to specify the referral percentage of the flat fee rate based on the referral agreement.

Handling different commission structures

Whether the referral fee is a flat amount or percentage-based, our tool can accommodate various structures. If multiple partners are involved, separate referral fee entries can be added.

Tracking and managing referral fee payments

You can specify who the referral fee is paid to, ensuring referral payments are correctly recorded and preventing disputes.

Also, you can manually update the payment status once a referral fee is completed, keeping all real estate referral fee payments organized and preventing any errors.

Ensuring compliance with referral agreements

Brokers and agents can upload signed referral agreements as part of the transaction record. This ensures that the referral fee is documented and aligned with the agreed terms.

Paperless Pipeline also allows you to create custom colored document labels, making it quick and easy to retrieve referral agreements.

Every change made to referral fees, payments, and commission adjustments is logged. This means brokers and auditors can track who made changes, when, and why, ensuring transparency and compliance with RESPA and regulations.

Generating reports for referral fee tracking

Our reporting tools enable you to generate detailed reports on total referral fees paid per agent or brokerage, unpaid or overdue fees, and referral fee trends over time.

Reports can be exported to accounting software, making it easier to reconcile referral fee payments with company financials.

The Ultimate Solution for Managing Real Estate Referral Fees

Referral fees are an essential part of the real estate industry, helping agents and brokers expand their networks and close more deals.

However, managing referral agreements, tracking payments, and ensuring compliance can quickly become problematic, especially as transactions scale.

That's where Paperless Pipeline's Commission Module comes in. Our platform simplifies referral fee tracking, automates commission calculations, and securely stores all agreements in one place.

If you're ready to take the hassle out of managing referral fees, sign up for a free Paperless Pipeline demo to see how our Commission Module can transform how you track and process real estate referral fees.