How To Set Real Estate Goals For A Thriving Brokerage

In today's unpredictable economic climate in the U.S., real estate brokers are under more pressure than ever to lead their teams with clarity and focus.

Fluctuating interest rates, low inventory, and shifting buyer behavior make it difficult to rely on past performance or market trends alone.

That's why setting and consistently tracking well-defined goals is no longer optional. It's essential.

Research shows that companies that set performance goals quarterly generate 31% more returns. Yet despite this advantage, only 51% of companies make the effort to align goals across their teams, and only 6% of them revisit those goals regularly.

If you want your brokerage to outperform the competition in the real estate industry, attract and retain top agents, and maintain steady growth through market turbulence, you need more than just a business plan. You need a productivity framework that keeps your team focused, aligned, and motivated.

In this article, we'll share nine practical tips for goal setting and productivity tracking that'll help your real estate business thrive, no matter what the market throws your way.

1. Set SMART Goals

Experts agree that your goals themselves are one of the most significant factors in your ability to achieve them successfully.

Goals that are defined in concrete and specific terms are more easily translated into action than vague hopes for the future.

Without definition and clarity, it's difficult to know if you've achieved success or to ensure that this goal supports your higher-level business objectives.

Instead, break high-level goals into actionable objectives and tasks that are clear and trackable.

The acronym SMART stands for specific, measurable, achievable, realistic, and timely.

The SMART goals framework is often helpful for turning goals into reality because it lays the path for achieving your objective within the goal itself.

Here are some examples of SMART real estate goals:

🎯 Specific

The goal is well-defined: "This quarter, I want to sign on as the buying agent with five families who will be looking to purchase a new house in my region within the next year."

For example, instead of saying, "We need more listings," a specific goal would be, "We want to secure three new seller listings in our target neighborhood by the end of the month."

📏 Measurable

Measurable goals mean that there are clear criteria and defined indicators for measuring and tracking progress and outcomes.

An example could be tracking the number of client consultations completed per week or measuring open house attendance with a sign-in sheet to see if your marketing efforts are working.

🏆 Achievable

As you define your goals, it's important to factor in how you will achieve them. Have others done this successfully before? What tactics have they used? What tools are available to you to help improve your chances of success?

As you develop your plan for achieving your goal, ensure all associated subtasks are also SMART.

For instance, if your brokerage has never closed more than 50 transactions in a year, a goal of hitting 100 may not be achievable in the short term. A more attainable goal would be increasing transactions by 15% to 20% using improved marketing tools.

✅ Realistic

It's essential to base your goals on the reality of your market. Spend some time looking into historical trends in your market and upcoming changes that may affect buyers' attitudes.

Economic trends, impending zoning changes, and countless other factors can spur or slow interest in the real estate market. Understanding what is currently happening can help you focus your goals appropriately.

If mortgage rates are climbing and inventory is low, it may not be realistic to double your buyer-side closings in the next quarter. A more realistic goal might be to maintain your current transaction volume while improving your average commission per deal.

⏰ Timely

Setting a time-bound deadline for achieving your goal can create a sense of urgency and motivate you to perform the necessary tasks to stay on track.

2. Get the Tools You Need to Stay on Track Easily

If you think of your goals as the endpoint on a map, you'll realize that you will still need a way to ensure you navigate your path successfully.

Paper lists can be somewhat helpful, but they have several downsides. They can become messy and disorganized as you make updates and changes.

They also don't provide any inherent functions or benefits that make it easy or desirable to track your progress and stick to your plan, and they're not flexible or dynamic.

Some platforms help you navigate the route to achieving your real estate goals. For example, if your goal for the year is to increase commissions, you'll need a plan to get from your current production level to your goal.

You'll need this, along with ways to ensure you're on track, well ahead of year-end, when you still have time to course-correct if your projections show a risk of underperforming.

Pro Tip:

With commission tracking, calendars, checklists, notes, automated reminders, and other easy-to-use features, Paperless Pipeline provides real estate brokerages, teams, and transaction coordinators with the tools they need to track every step of the goal-setting process easily.

Accessible from any computer or mobile device, these features support all of the imperatives of SMART goals.

Once you define your objectives, you can set them up within Paperless Pipeline and track and measure your progress.

As progress moves forward, so do the transaction completion percentages.

And as your goals evolve, you can easily make updates and compare current and historical performance to see just how far you've come.

3. Make the Process Fun and Satisfying

Although tracking your goal-setting productivity can be a powerful incentive for staying on track in your real estate career, this can feel like a slog or fall to the wayside when you have properties to show and transactions to close.

But status reports shouldn't be yet another task you have to remember to perform, as this can add even more perceived work to the process and reduce the likelihood of sticking to your plan.

On the other hand, receiving updates about how well you are doing can add excitement and motivation that propels you to the next milestone, or incentivize you to try some new tactics for growing your pool of listings. For example, if your annual sales targets look like they could fall short.

Pro Tip:

Paperless Pipeline's automated production reports can be a motivating tool. They deliver information right to your inbox about how the company and your real estate agents are progressing toward common goals.

4. Align Individual Goals with Team and Brokerage Objectives

One of the most common pitfalls in goal setting is misalignment between individual real estate agent goals and the overarching vision of your own business.

A top-producing agent may set a personal goal of increasing luxury listings, while your brokerage's strategic priority may be expanding your presence in suburban neighbourhoods.

When goals aren't aligned, your efforts can become fragmented and less impactful.

As a broker, start by clearly defining your business's strategic priorities for the quarter of the year. These could include increasing market share, expanding into a new region, boosting lead generation, or improving agent retention.

Then, hold one-on-one meaningful conversations with each team member to help them define realistic goals for a successful career that supports the bigger picture.

For example, if your brokerage aims to close 200 residential sales this year, the agent's SMART goals might be to close 15 single-family homes in your area and make 50 prospecting calls (or at least define how many calls it will take to reach this goal).

You could also make it their goal to improve their marketing efforts, attend community events to meet potential clients, or get in touch with 10 past clients to follow up.

5. Break Down Big Goals into Weekly or Monthly Milestones

Large, ambitious goals like doubling annual sales or onboarding 10 new agents can be motivating but also daunting. Without clear milestones along the way, agents and team members can lose focus or get discouraged.

Breaking down big goals into smaller, time-bound targets makes them more manageable and easier to track. For example:

- Instead of sales goals like "Close 50 transactions this year," break them down to "Close four to five transactions per month" and determine how many appointments would be needed to meet this goal.

- Instead of "Recruit 10 new agents," track progress weekly and aim for "Reach out to five potential recruits this week."

- Instead of "Expand our digital marketing and social media presence to get more listings," you could aim to "Publish two posts to Facebook per week."

6. Use Data to Set Realistic Goals

Setting goals based on ambition alone isn't enough. You need historical and market data to guide expectations and help real estate professionals meet their career goals.

Too often, brokers or agents pick numbers that sound good without considering prior performance, seasonal market trends, or economic indicators.

Start by reviewing:

- Your team's production for the last 12 to 24 months.

- Average days on market (DOM) in your area.

- Seasonality patterns.

- Local economic housing trends.

- Individual agent close rates and average transaction sizes.

By looking at hard data, you can create goals that are both aspirational and realistic.

Pro Tip:

Use Paperless Pipeline's robust reporting features to pull past performance data by agent, team, or transaction type. Compare this with market data to build realistic, informed goals for each role in your brokerage.

7. Review Progress Regularly, Not Just at Year End

One of the biggest mistakes real estate teams make is setting goals at the beginning of the year and never reviewing them again. Without regular reviewing, even the best plans can go off course.

Build in monthly or quarterly goal reviews with your team and use check-ins to assess what's working and what isn't.

Ensure you celebrate progress and wins, adjust goals based on new market realities, and provide support or training where agents may be falling behind to help them build confidence.

8. Incentivize Progress with Recognition and Rewards

Motivation plays a significant role in whether the right goals are achieved or forgotten. Beyond financial compensation for closing deals, recognition and team-based rewards can help them stay focused and drive consistent effort toward actionable goals.

Some examples include:

- Offer a monthly spotlight for the real estate agent who makes the most progress toward a specific goal.

- Create a leaderboard for the most listing appointments, closings, or new recruits.

- Set up team-wide incentives like team dinners or outings if shared targets are met.

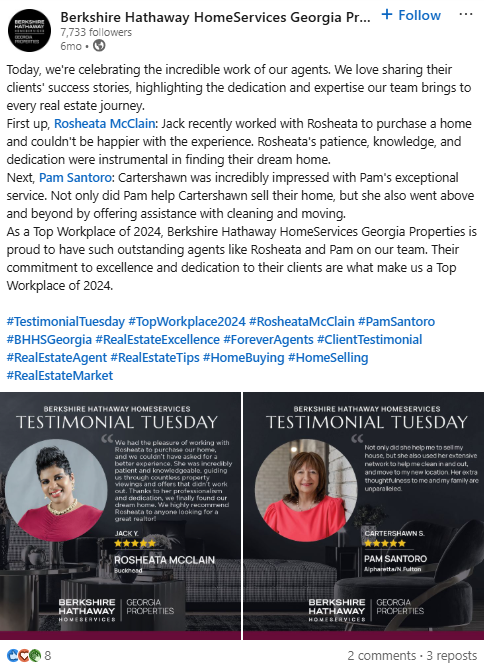

You could also celebrate your team on social media. This brokerage regularly posts shoutouts of their top-performing agents to celebrate their progress:

This turns goal tracking into a cultural habit within your real estate business and makes performance visible and valued.

9. Build a Solid Foundation with Process-Driven Goal Setting

Before setting ambitious sales or recruitment targets, it's crucial to ensure that your operations are built on a solid foundation.

Without reliable systems and clear workflows in place, even the most motivated teams with enough leads can struggle to achieve their goals consistently.

Start by auditing your current processes:

- Are your transactions being tracked accurately?

- Do agents have a clear understanding of what's expected of them?

- Are checklists, timelines, and communication protocols standardized across your team?

By streamlining your transaction management, communication, and reporting processes first, you eliminate bottlenecks, reduce the risk of goals falling through the cracks, and help your team stay motivated.

Pro Tip:

Paperless Pipeline helps you build this solid foundation by centralizing task management, automating routine workflows, and giving brokers and agents full visibility into what's happening across every transaction. With this in place, you can confidently set and scale your real estate goals.

Turn Goals into Growth and Set Your Brokerage Up for Success

No matter the state of the market, success in real estate doesn't happen by chance. It's the result of intentional, focused effort.

Setting meaningful goals gives your brokerage direction, and tracking them keeps your team accountable. Additionally, aligning your goals with real-time performance data transforms them from abstract ideas into measurable business growth.

Paperless Pipeline gives real estate brokers, teams, and transaction coordinators the tools they need to set, track, and achieve their goals with clarity and confidence.

With commission tracking, automated reports, customizable workflows, and real-time visibility into team performance, you can stay focused on what matters and adjust quickly when the market shifts.

Start your free 14-day Paperless Pipeline trial today to see how you can set your goals, track your progress, and hit your targets with ease.